As an AT&T employee, one of the most significant decisions you will face regarding your retirement is how to manage your pension. This decision is particularly influenced by factors beyond your control – like fluctuating interest rates.

For those nearing retirement, understanding the impact of interest rates on your pension is crucial when planning the best time to retire and the most suitable AT&T pension plan – and could make the difference of thousands of dollars in your lump sum payout.

In this blog we will explain the relationship between interest rates and pension payouts so you can make more informed decisions that align with your financial goals.

The connection between interest rates and AT&T pension payouts

Before we address how interest rates impact pension payouts, it’s important to understand how AT&T determines pension payouts. AT&T calculates its pension payouts using the Composite Corporate Bond Rate, which moves in step with general interest rates, such as those tied to loans and credit cards.

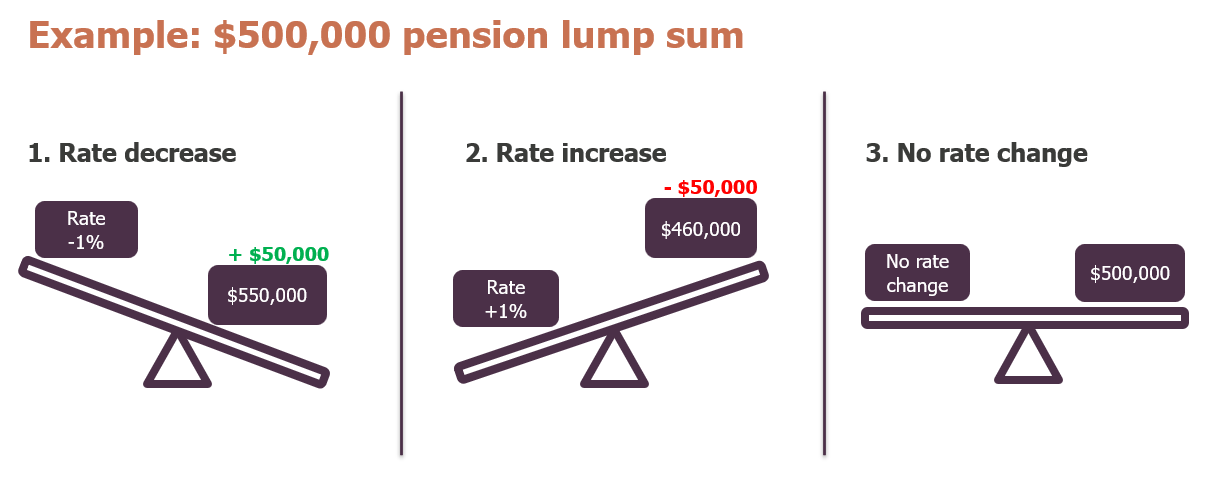

There is an inverse relationship between this rate and your lump-sum pension payout. Meaning that as interest rates rise, lump-sum payouts decrease, and as rates fall, lump-sum payouts increase.

How changing interest rates could influence your retirement timing

Interest rates can change throughout the year. While we can’t predict exactly when or by how much, they often shift over time as market conditions evolve. However, we do know that AT&T uses the November Corporate Bond Rate to set the pension calculation for the following year.

So, if interest rates drop this November, it could result in a larger lump-sum pension payout for next year. Conversely, rising rates can lower your payout.

This is why it is important to stay informed about rates and consider timing your retirement accordingly.

Here are three key considerations for AT&T employees when deciding when to retire:

- Should You Retire Sooner or Later? In a scenario where interest rates are predicted to decline in the upcoming year, waiting a bit longer could result in a larger pension payout, as the lower rate translates to a higher lump sum.

On the other hand, if the rates stabilize or you have other financial or lifestyle needs, retiring sooner may still be advantageous. The best decision depends on your financial goals and personal situation. - Lump-Sum vs. Monthly Annuity: AT&T offers the option of taking your pension as a lump sum or as a monthly annuity. In a declining rate environment, a lump sum becomes more attractive, as the payout amount increases. You can roll it over into an IRA and manage it as you see fit.

A monthly annuity, however, provides a steady income stream for life, unaffected by interest rate fluctuations, but without a cost-of-living adjustment to combat inflation. The right choice depends on your need for flexibility, your tolerance for investment risk and your income requirements in retirement. - Other Retirement Income Sources: Whether rates rise or fall, or even stay the same, you may need to adjust how you plan to draw from other retirement income sources, like your AT&T 401(k) or Social Security.

For example, waiting to take your pension when rates drop and payouts rise might allow you to delay Social Security, which could increase your monthly benefit over time. Balancing these income sources is a key part of building a sustainable retirement strategy.

The bottom line for AT&T employees

Ultimately, deciding when to retire and which AT&T pension payout option to choose is deeply personal and depends on many factors – your financial goals, other income sources, current market conditions and interest rates, to name a few.

Wherever rates go next, it’s essential to balance this change with your overall retirement plan and financial goals.

Working with an AT&T-experienced financial adviser can help you make a confident and informed decision about when to retire and how to best utilize your AT&T retirement benefits. Schedule a free consultation today!

If you’d like to learn more about using your AT&T pension, AT&T 401(k) and other AT&T benefits for retirement, downloading a copy of The AT&T Employee's Guide To Retirement here and share it with a colleague who might find value in it too!

Disclosure; Although ACM does not charge a fee for downloading the report, it is intended to result in you establishing an advisory relationship with the firm.

{kind=link}