On the list of top retirement planning goals, long-term care funding for many people is probably near the bottom. Who wants to think about spending time in a nursing home instead of time in a vacation home? But as the life expectancy of older adults rises, almost everyone should consider having some kind of plan in place.

Long-term care refers to a range of services to meet the personal health care needs of someone suffering from chronic illness or disability over an extended period of time. Primarily, this type of care consists of help with daily activities, such as eating, bathing, dressing, etc. Care is provided at home, in an assisted living facility or in a nursing home.

The need for long-term care can dramatically change your life as well as the lives of people close to you.

So, when should you start planning for long-term care? Like your other retirement planning needs: the earlier, the better. Many people though don’t start until they’re in their 50s. If planning for long-term care isn’t yet on your radar, these facts should do the trick.

YOU OR SOMEONE YOU LOVE WILL LIKELY NEED LONG-TERM CARE

An estimated 70% of people reaching age 65 today will need some form of long-term care in their lifetime, according to the U.S. Department of Health and Human Services. One-third of today's 65 year-olds may never need long-term care support, but 20 percent will need it for longer than 5 years.

Therefore, there’s a good chance you or someone you love will be affected.

The growing demand for long-term care can be attributed to the fact people live longer. With age comes greater risk of experiencing debilitating conditions, like strokes and dementia, that leave individuals especially vulnerable.

LONG-TERM CARE IS EXPENSIVE

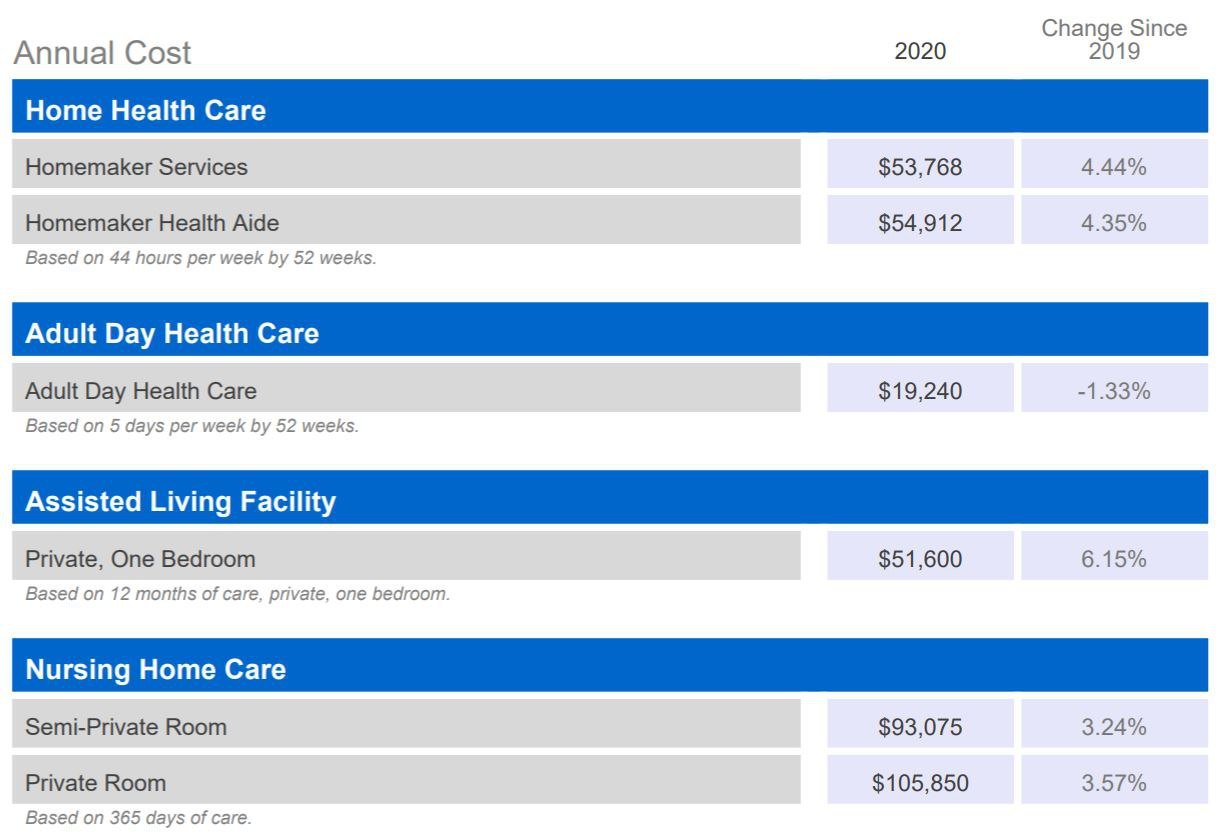

Long-term care costs vary based on the services provided, where care is provided and how long care is provided. According to the latest Genworth Cost of Care Survey, the national median hourly rate for care at home by a homemaker service is $23.50, and $24 for a home health aide. Annually, the median cost of these services add up to $53,768 and $54,912, respectively, assuming 44 hours of care per week.

Outside the home, care at an assisted living facility may cost around $4,300 per month, for a yearly median cost of $51,600. Nursing home costs differ between semi-private and private rooms, with the national median daily rate at $255 and $290, respectively. That works out to a median annual cost of more than $93,000 annually for a semi-private room and more than $105,000 annually for a private room.

Source: Genworth, Cost of Care Survey 2020

The high cost of long-term care is why many people often find themselves relying on family and friends to provide care, which can create a financial, emotional and physical burden on loved ones.

MEDICARE DOESN’T COVER LONG-TERM CARE

A common misconception is that older adults can rely on Medicare for long-term care needs. But, Medicare pays for “medical services,” whereas long-term care primarily consists of “custodial services.”

Medicare provides support only on a limited basis for skilled services in a nursing home or at a patient’s residence, with a maximum benefit period of 100 days. However, full benefits last only 20 days. Considering most recipients need care for one to three years, Medicare is not a viable option to cover long-term care expenses.

YOU LIKELY WON’T BE ABLE TO GET INSURANCE IF YOU WAIT

Long-term care insurance is one way to hedge against the high cost of care. Basically, long-term care insurance pays a daily amount, up to a predetermined limit and length of time, for qualified services. Those factors, along with any optional benefits, generally determine the cost of premiums.

Age and current health, however, are also major factors. The average long-term care insurance buyer is age 57, with most policyholders falling in the range of ages 55-64. The older a person is, the more expensive the policy will be. Insurers can also reject or place care limitations on those who are in poor health or have preexisting conditions.

QUALIFYING FOR MEDICAID MEANS LIQUIDATING MOST OF YOUR ASSETS

Generally, Medicaid is for those who have limited savings and cannot afford long-term care insurance or were denied coverage. Typically, to qualify for Medicaid, an individual is only allowed to have $2,000 in countable assets. For married couples, the spouse who isn’t applying for Medicaid benefits may keep up to half of both spouses’ joint liquid assets, but only up to $130,380 (2021) in what is called the “community spouse resource allowance.” It’s important to note that Medicaid qualification guidelines vary from state to state and may change from year to year. Some state allowances are much lower.

Still, some people try to reposition their assets to work around Medicaid limitations and gain access. However, such Medicaid planning techniques have been made more difficult as states limit the transfer of assets to avoid using them to pay for long-term care. So-called ‘look back’ rules prevent people from gaming the system by requiring assets to have been liquidated a certain amount of years prior, usually five years, to applying for Medicaid. Further, federal law requires states to collect from a person’s estate the costs of the Medicaid benefits received.

For information on ways to cover the costs of long-term care, download our white paper “Options for Funding Long-Term Care Expenses.”

{kind=link}