On the Richter scale of financial fears, most people would put a recession near or at the top. From job loss to market downturn, the potential magnitude of financial dangers can be severe. But just how fearful should investors be of the next recession? The fact is recessions are a normal feature of the business cycle.

Therefore, a better question to ask is: How do you build a recession-proof portfolio?

Historically, the stock market has weathered every recession, and there’s no reason you can’t do the same.

How common are recessions?

The National Bureau of Economic Research (NBER) defines a recession as “a significant decline in economic activity spread across the economy, lasting more than a few months.” It is commonly declared when Gross Domestic Product (GDP) shrinks for two consecutive quarters (six months), businesses cease to expand, the rate of unemployment rises and housing prices decline.

There have been 12 recessions since 1945. That means a recession has occurred at least once every 10 years. What is most important to note is that recessions don’t last long – only around 10 months on average. By the time we know a recession is here, we’ve already been in one for six months, so it is likely already halfway over. In other words, it’s too late to start trying to time the market.

How a recession impacts the stock market

Conventional wisdom says a recession invariably means a severe market downturn. The stock market, however, is not the economy. Even though it is said the stock market is the collective view of the economy’s future, they are not perfectly correlated. Especially, when it comes to recessions. Each recession is unique. Whether the market crashes, like in 2008, depends on the causes and severity of the recession.

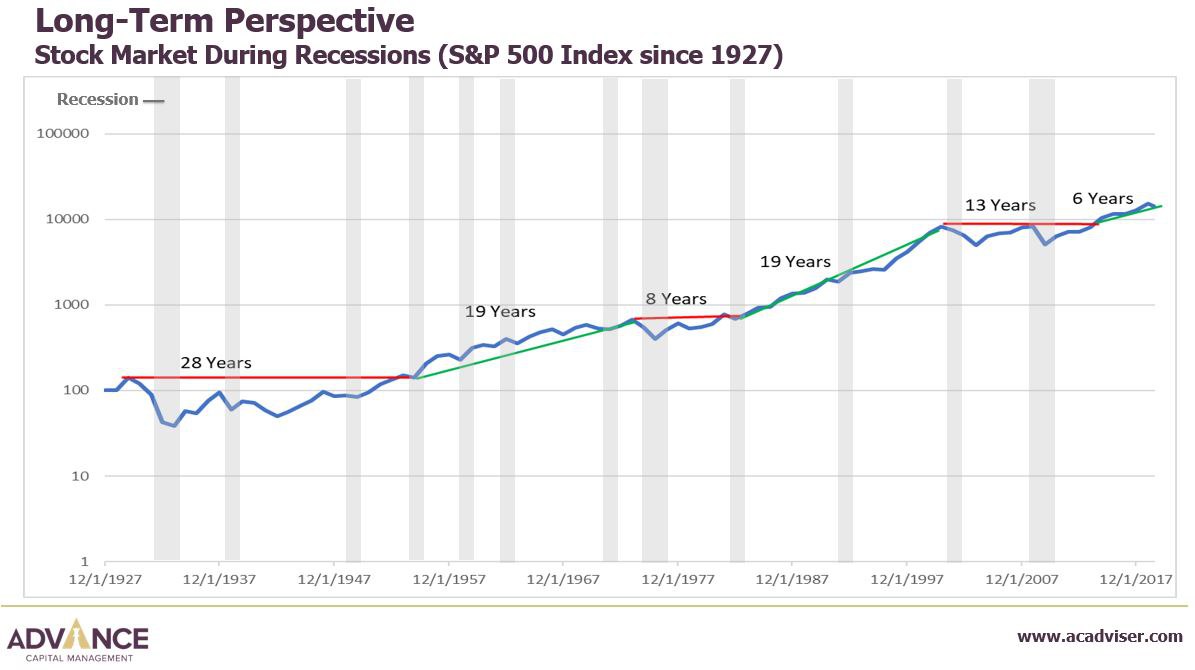

The chart above illustrates the cycles of the stock market, as represented by the S&P 500, dating back to 1927. Every down or sideways period is followed by a period of positive growth. The gray bars indicate every recession along the way. As you can see, recessions have occurred at all phases of the market cycle, during market expansions and downturns, and during the beginning, middle and end of each type of cycle.

What we can learn from this is that a market downturn is not a sign of an impending recession, nor does a recession mean a stock market decline. Further, just because the stock market is expanding doesn’t eliminate the possibility of a recession.

Simply put: Recessions don’t discriminate when it comes to the market, and the market doesn’t always care what the economy is doing. With that said, predicting a recession and its impact on the stock market is nearly impossible.

Steps to recession-proof your portfolio

The key to investing before, during and after a recession is to keep a long-term perspective and focus on the big picture. Instead of trying to time your way in and out of various parts of the market or individual investments, you build a portfolio that will carry you for the long haul.

Aggressive market-timing moves, such as shifting your portfolio to cash, can backfire. Some of the biggest gains can happen at the tail end of an economic cycle or immediately after a market bottom. It’s often better to stay invested to avoid missing out on the gains from the recovery.

Following are the building blocks for a long-term portfolio.

Diversified investments

Some sectors of the stock market, such as consumer staples and companies with long histories, have traditionally been safe bets during economic downturns. However, it is dangerous to load up on one particular sector. Should a recession coincide with a market downturn, it is difficult to know what investments will be most affected.

This is why diversification – owning investments across a variety of asset classes – is a long-term investment strategy that is especially useful during a recession. It eliminates the guesswork and helps reduce risk, as the winners make up for the losers. Essentially, diversifying your assets can act as a restraint on portfolio losses.

Asset allocation aligned with your goals

We know that stocks typically perform poorly during recessions. Yet, trying to time the market by selling stocks often does more harm than good. Does that mean investors should do absolutely nothing? Of course not.

You can prepare for a recession by reviewing your overall asset allocation, which may have changed significantly during the bull market, to ensure that your portfolio is balanced, broadly diversified and, most importantly, aligned with your specific long-term financial goals.

What asset allocation is right for you depends on personal factors, including your objectives, age, savings and income, current assets and attitudes toward risk. To have enough time to build wealth through good times and bad, you need a mix of investments that you’re comfortable sticking with for the long haul.

A balanced portfolio of highly changeable investments like stocks with relatively steady investments like bonds generally makes for a smoother, consistent ride. The objective is to have enough risk in your portfolio to generate the growth you need to achieve your goals, but not enough risk to suffer deep losses or to tempt you into ill-timed changes when the market fluctuates.

As advisers who provide personalized investment advice, Advance Capital Management doesn’t make blanket asset allocation recommendations. However, those nearing retirement should generally have more conservative asset allocations to help preserve more money. Younger individuals, on the other hand, have the luxury of time to recoup any losses and capture more of the upswing, and should therefore consider an aggressive asset allocation.

Flexible withdrawal rate

As you prepare to retire, your withdrawal strategy is an important part of managing your portfolio for the long term.

An undesirable scenario is that you retire into a weak market environment and withdraw from a portfolio that’s simultaneously declining. Spending down in a down market can leave less of your portfolio in place to recover once the market does. This may lower the probability that your portfolio will last as long as you need it to.

One way to bypass that danger is to maintain a flexible withdrawal rate. For example, suppose you plan to withdraw 5% of your portfolio each year. In a downturn, you may temporarily lower that rate by half to one percent while relying more on other sources of retirement income (pension, Social Security, etc.) and/or reducing your expenses. As market conditions improve, you can then raise your withdrawal amounts.

By taking modest withdrawals, less than your expected amount, if possible, in those beginning weak years, you can help preserve some of your balance. It also puts you in position to possibly spend more during those strong years.

Final thoughts

The best way to prepare for a recession is to make sure in advance that your portfolio is aligned with your personal goals and designed to be balanced enough to benefit from periods of growth before it happens, while resilient during those inevitable periods of volatility.

Of course, your financial life is bigger than just your portfolio. You also have to think about what financial planning steps you need to take to help get you through times of economic turbulence. For a more comprehensive overview of preparing for a recession, be sure to download our guide: Protecting Your Money Against a Recession

{kind=link}