The average retirement age in America differs from state to state, ranging from 62 to 65, according to the U.S. Census Bureau. The decade before retirement – your 50s – isn’t time to coast like a teen suffering from senioritis. You should still be pursuing your dreams – and taking important steps to financial freedom.

The average retirement age in America differs from state to state, ranging from 62 to 65, according to the U.S. Census Bureau. The decade before retirement – your 50s – isn’t time to coast like a teen suffering from senioritis. You should still be pursuing your dreams – and taking important steps to financial freedom.

Even if you’ve lived a full life thus far, many adults don’t experience their greatest achievements until they’re older. Consider the career change of a research assistant at the Office of Strategic Services during World War II. She married a foreign service officer, and while stationed in Paris, developed a love for cooking French cuisine. After years of honing her culinary skills, she published her first cookbook at age 49 and made her television debut, as “The French Chef,” at age 51. Her name was Julia Child.

Or, how about the story about a hapless businessman, who at age 65 found himself left with only his meager savings, Social Security check and a recipe for fried chicken he developed when he was 50. With that “secret recipe,” he built one of the most successful fast food franchises in America. His name was Harland Sanders, better known by his honorary title of colonel.

The point is that in your middle and later years, there is still so much more you can accomplish. The world is your oyster. And, the same goes for your retirement savings. Even if you’re far ahead of the game or haven’t even gotten started, now’s the time to get financially in shape.

Why Your 50s Are Financially Important

As you turn age 50, you should apply the same focus on pursuing your passions to managing your finances. You’ll likely retire from your current job in just the next 10-15 years. And, that transition may happen voluntarily or not.

In your 50s, you have time to either catch up or boost your savings. Whether you choose to continue to work in retirement or not, is your choice. You still need to take the appropriate steps now to ensure you will have enough income to support you for the next two or three decades, or longer.

5 Steps to Financial Freedom

The good news is that whether you’re just beginning to save for retirement or have been since the first day on the job, the steps you should take are essentially the same. Here are five steps to financial freedom to take in your 50s:

- Determine your number.

How much do you need to retire? Few do the math. An astounding 81% of Americans don’t know how much they need to retire, according to a study by Bank of America Merrill Lynch.

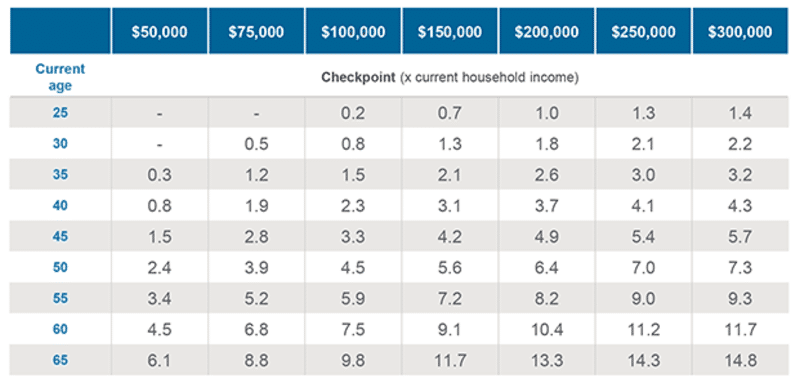

A simple way to determine if you’re on track and how far you have to go, is to look at the retirement savings checkpoints in the chart below. It assumes you plan to maintain an equivalent lifestyle in retirement. Simply multiply your salary by the checkpoint shown that corresponds to your age.

For example, a 40-year-old with a household income of $100,000 should have $230,000 ($100,000 x 2.3) saved for retirement.

Source: JP Morgan (Model assumptions: annual gross savings rate: 10%; pre-retirement investment return: 6%; post-retirement investment return: 5%; inflation rate: 2.5%; retirement age: 65 (primary earner) and 62 (spouse); years in retirement: 30).

- Make catch-up contributions

At age 50, you qualify for catch-up contributions, an extra amount that you’re legally allowed to contribute into your retirement accounts. You save up to an additional $6,000 in an employer-sponsored plan and up to an additional $1,000 in a Traditional or Roth IRA. Catch-up contributions can either help you get on track or give your retirement savings an added boost.

- Ensure your health needs will be covered

Healthcare will likely be one of your largest expenses in retirement, costing as much as $266,000 in Medicare premiums alone, according to one estimate. At age 65, you will be required to sign up for Medicare. But, there are many things Medicare does not cover. Therefore, you should consider how you will pay for future healthcare costs sooner rather than later. Research supplemental coverage options and find out if you’re eligible for retirement benefits other than Medicare.

- Determine what you want to do in retirement

What are you going to spend your retirement savings on? The answer may be harder than you think.

You may have big dreams, such as traveling or writing a book, but they might not be enough to keep you busy. How are you going to replace those 40-50 hours per week that you currently spend working? Because of rising life expectancies, you can reasonably expect retirement to last 20-30 years. That’s a lot of free time. You don’t want to make the mistake of spending money frivolously in a pursuit to just find out what makes you happy in retirement.

- Get your estate in order

Whether you plan to leave a legacy or not, there are two crucial estate steps you should take: create a will and designate a power of attorney. It’s never too early to take these steps because something could happen to you at any moment. These documents can help protect your assets and your family’s well-being.

But wait, there’s more!

From choosing the right age to claim Social Security to figuring out where you want to live, there are many more important financial steps to take in your 50s to help you realize your dreams. You can find them in our free ebook, Your Money in Your 50s: A Retirement Planning Guide for Procrastinators and Avid-Savers. Click the link or the image below to download it now:

{kind=link}